The latest commercial property price report from MSCI Real Capital Analytics said that multifamily property prices in May fell 0.9 percent from their level of the month before and fell 12.5 percent from their level of one year before. These were the largest month-over-month and year-over-year rates of decline of any of the commercial property types tracked in the report. However both rates of decline were less than those experienced last month.

Defining CPPI

MSCI tracks an index called the Commercial Property Price Index (CPPI). The index is computed based on the resale prices of properties whose earlier sales prices and sales dates are known. The index represents the relative change in the price of property over time rather than its absolute price. Note that, as new properties are added to the MSCI dataset each month, they recalculate the CPPI all the way back to the beginning of the data series.

General price decline continues

Prices for industrial property, fell 0.5 percent for the month, matching last month’s decline. Suburban offices property prices fell 0.7 percent for the month. Retail property prices fell 0.6 percent.

Office properties within central business districts (CBDs) were again the best performer, experiencing a price decline of only 0.4 percent. However, the relatively good recent performance for this property type may be because prices for these properties have been depressed. Offices in CBD’s is the worst performing of the commercial property types tracked by MSCI over the past three-year and five-year time spans.

All property types tracked also saw price declines on a year-over-year basis. Industrial property was the best performing with a price drop of 2.3 percent. Prices for offices within CBD’s were down 6.9 percent while prices for suburban offices fell 8.1 percent. Prices for retail property were down 7.4 percent.

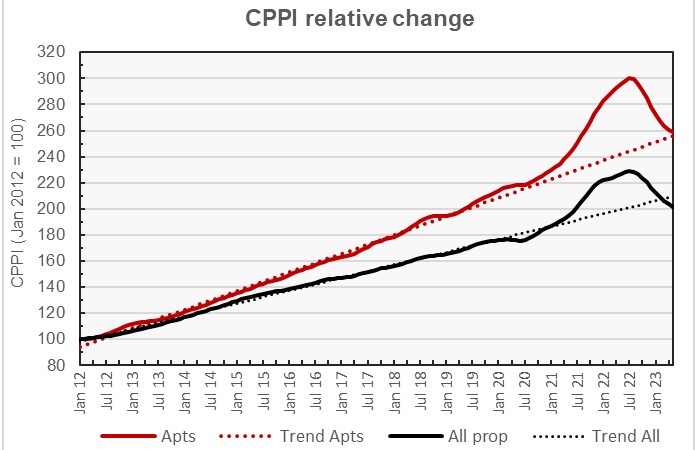

CPPI returns to trend

The first chart, below, shows how commercial property prices and multifamily property prices have changed since January 2012. To simplify the comparison, both CPPI’s have been normalized to values of 100 in January 2012. The chart also contains trend lines showing the straight-line average rates of price appreciation for the two asset classes based on their performance from January 2012 to December 2019.

The chart shows that recent price declines have brought pricing back close to the previous trend lines. Multifamily property prices are currently about 1 percent above the pre-pandemic trend while pricing for all commercial property as a single asset class is currently about 4 percent below trend.

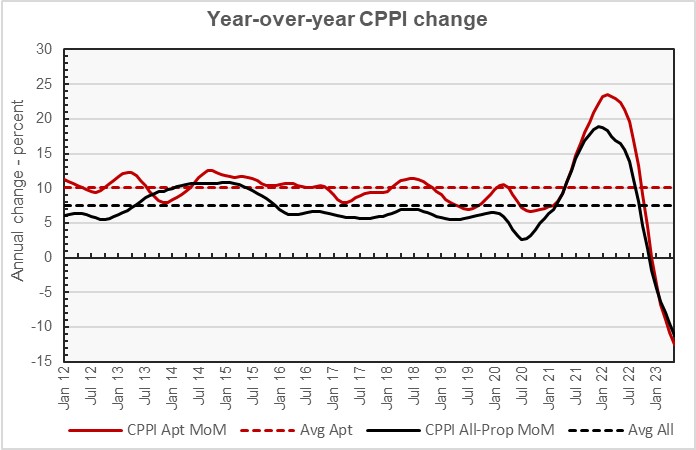

The next chart plots the year-over-year changes in the values of the CPPI’s since January 2012 for all commercial property as a single asset class and for apartments. The chart shows that annual price changes stayed within close ranges between January 2012 and January 2020. Since then, annual price changes first surged and then plunged. Year-over-year price changes are strongly negative and currently show no sign of returning to growth.

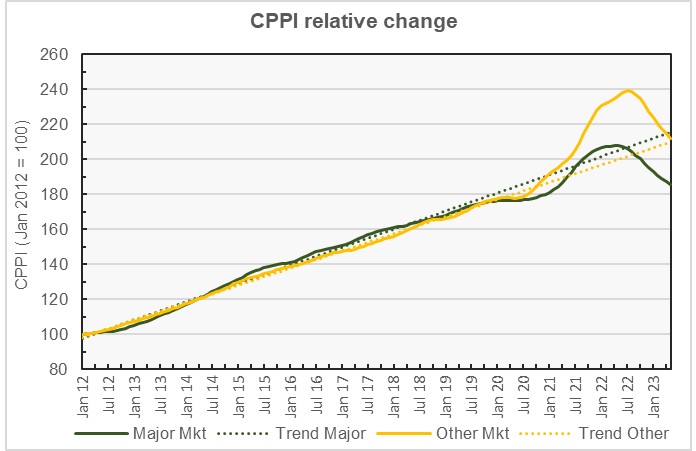

Major metros falling further below trend

The MSCI report provides data comparing the price changes of commercial property in 6 major metro* areas against those in the rest of the country, although it does not separate out apartments from other commercial property types in this comparison. The next chart, below, plots the history of the price indexes since January 2012 for both market segments along with trend lines based on straight-line fits to the changes in these between January 2012 and December 2019.

The chart shows that property prices within the major metros dipped more strongly in the early months of the pandemic than did the prices for other metros. Major metro prices also did not get as large of a late-pandemic bump as did prices in other metros. Major metro prices are now 14 percent below their trend. Meanwhile, prices in other metros are still 1.1 percent above their long-term trend.

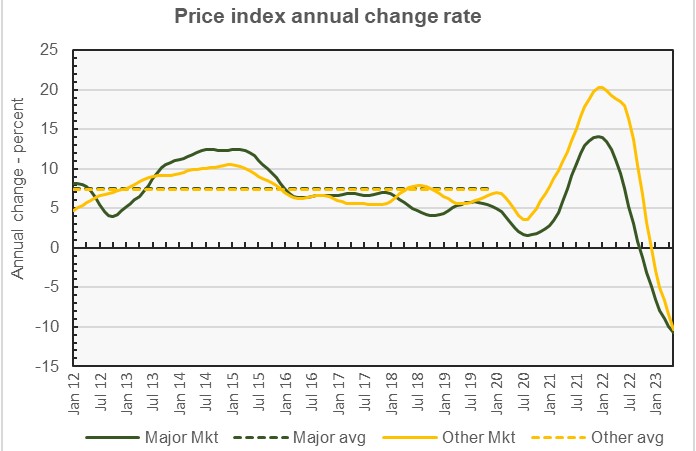

The final chart plots the history of the year-over-year change in the price indexes for the two property markets since January 2012. The chart shows that year-over-year price appreciation for the major markets turned negative earlier than did price appreciation of the other metros. However, the year-over-year rate of price declines for the other markets has now nearly caught up with that for the major markets. The chart also plots the average rate of year-over-year price appreciation for the two asset classes for the period from January 2012 through December 2019.

By the numbers, price appreciation for commercial property in major metros was reported to be -0.9 percent for the month and -10.7 percent for the year. Price appreciation for commercial property in non-major markets was reported to be -1.3 month-over-month and -10.3 percent year-over-year. The long-term pre-pandemic average rates of appreciation are 7.7 percent for major metros and 7.4 percent for other metros.

The full report provides more detail on other commercial property types. Access to the MSCI report can be obtained here.

*The major metros are Boston, Chicago, Los Angeles, New York, San Francisco and Washington DC.