Fannie Mae’s July economic and housing forecast reflects the surprising strength of the U.S. economy in early 2023. It predicts a higher level of multifamily starts and single-family starts in both 2023 and 2024 than did earlier forecasts.

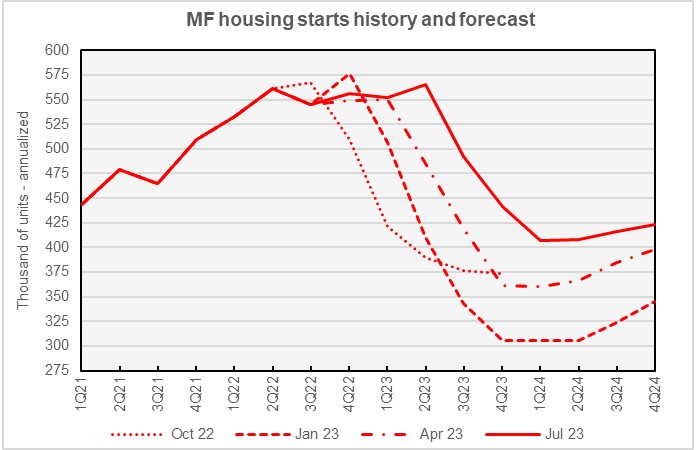

Multifamily starts downturn to come later

The current forecast for multifamily housing starts is shown in the first chart, below, along with three other recent forecasts. Fannie Mae considers any building containing more than one dwelling unit to be “multifamily”, including both condominiums and rental housing units.

The chart shows that the forecasters have had to repeatedly delay the date at which they expect the current high level of multifamily housing starts to fall. In the commentary that accompanied the forecast, Fannie Mae’s forecasters pointed to the lack of homes for sale as supporting the new construction of all types of housing, including multifamily. The lack of homes for sale was attributed to the mortgage lock-in effect, where homeowners are reluctant to give up the mortgages they obtained during the recent long period where mortgage interest rates were exceptionally low.

In addition, the unusually strong upward revision in the third estimate of first quarter GDP caused Fannie Mae to upgrade its outlook for 2023.

The July forecast for multifamily starts was higher for every quarter from Q2 2023 through 2024 than was nearly any previous forecast. The largest quarterly revision from last month’s forecast was for Q4 2023, with an upward revision of 43,000 units, annualized. The lowest annualized rate of multifamily housing starts is now predicted to be 407,000 units in Q1 2024.

Compared to last month’s forecast, the predicted number of multifamily starts in 2023 was revised upward by 29,000 units to 512,000 units. The predicted number of multifamily starts for 2024 was revised upward by 26,000 units to 414,000 units.

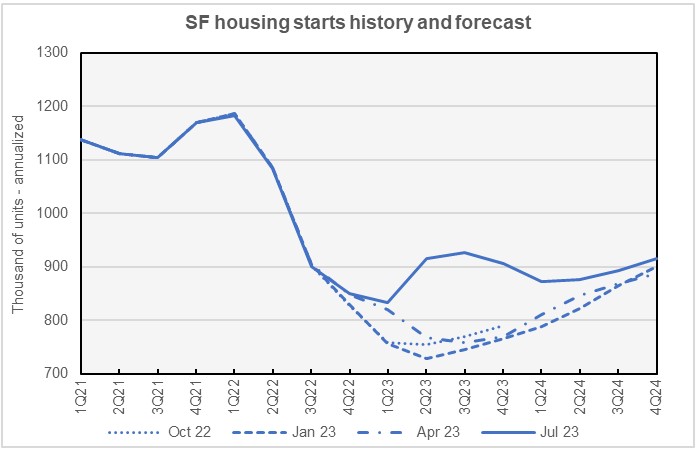

Bounce expected in single-family

The current forecast for single-family housing starts is shown in the next chart, below, along with three other recent forecasts.

As with multifamily, Fannie Mae’s forecasters raised their predicted numbers for single-family starts over the entire forecast horizon, compared to last month’s forecast.

Fannie Mae now expects single-family starts to be 896,000 units in 2023, up 72,000 units from the level forecast last month. Fannie Mae now expects single-family starts to be 890,000 units in 2023, up 45,000 units from the level forecast last month.

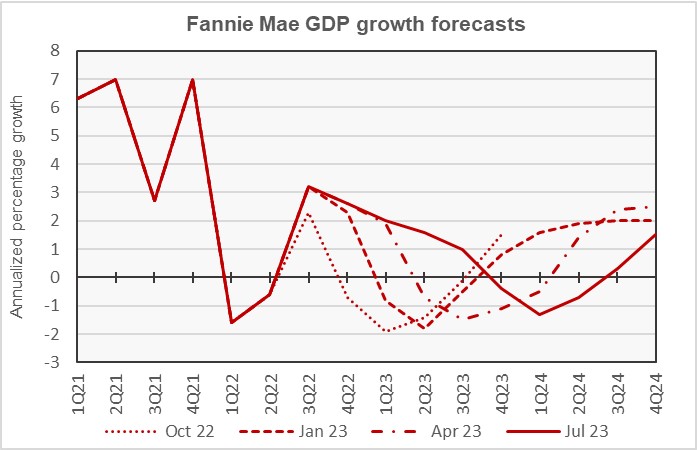

Later GDP downturn, later recovery

The next chart, below, shows Fannie Mae’s current forecast for Gross Domestic Product (GDP) growth, along with other recent forecasts.

Fannie Mae’s forecasters have slightly delayed the date of the expected recession compared to other recent forecasts. They now expect the first quarter of negative GDP growth to be Q4 2023, the latest date they have ever predicted. The greatest economic contraction is now expected to occur in Q1 2024 with negative growth of 1.3 percent, annualized. Positive GDP growth is expected to return in Q3 2024, also one quarter later than in other recent forecasts.

The full year forecast for GDP growth for 2023 was revised upward by a full percentage point to 1.1 percent. The full year forecast for 2024 was revised downward by 0.9 percentage points to -0.1 percent.

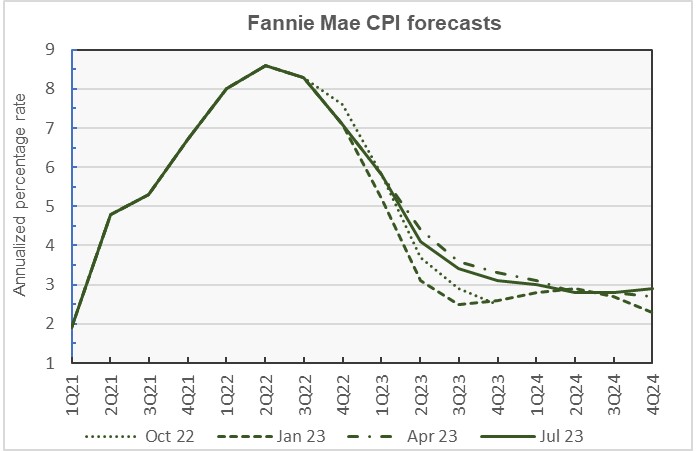

Inflation forecast edges lower

The next chart, below, shows Fannie Mae’s current forecast for the Consumer Price Index (CPI), along with three other recent forecasts.

The current Fannie Mae inflation forecast follows the same pattern as last month’s forecast, with a steady decline in headline CPI through Q3 2024 with a 0.1 percentage point bump upward in Q4 2024. However, the current forecast has CPI running higher in late 2023 and early 2024 than did last month’s forecast. The largest revision was for Q1 2024 where the inflation forecast was raised by 0.3 percentage points, annualized.

Looking at whole-year forecasts, the forecasts for year-over-year CPI growth in Q4 2023 was revised upward from last month’s level by 0.2 percentage points to 3.1 percent. The Q4 2024 inflation forecast was left unchanged at 2.9 percent.

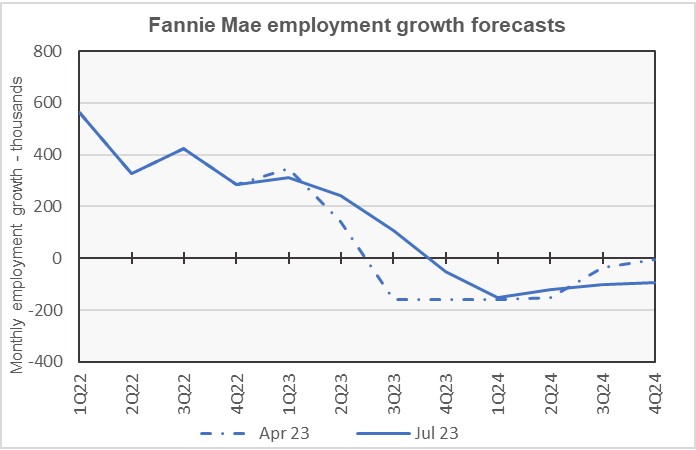

Job growth higher in 2023

The next chart, below, shows Fannie Mae’s current forecast for employment growth, along with the forecast from 3 months earlier. Employment growth is our preferred employment metric since job gains, along with productivity gains, drive economic growth.

Compared to the forecasts made since the population base was revised in February 2023, Fannie Mae’s July employment growth forecast calls for the highest number of job gains for 2023 and the highest number of job losses for 2024.

The first quarter with declining employment levels is still expected to be Q4 2023, but the expected job losses in that quarter are predicted to be lower than foreseen last month.

Compared to last month’s forecast, the expected full year forecast for employment growth in 2023 was revised upward from a gain of 1.4 million jobs to a gain of 1.8 million jobs. The employment growth forecast for 2024 was revised from a loss of 900,000 jobs to a loss of 1.4 million jobs.

The Fannie Mae forecast can be found here. There are links on that page to the detailed forecasts and to the monthly commentary.