Fannie Mae’s September economic and housing forecast predicts higher multifamily starts in 2023 but lower multifamily starts in 2024 than called for in last month’s forecast.

Multifamily starts expected to slow – later

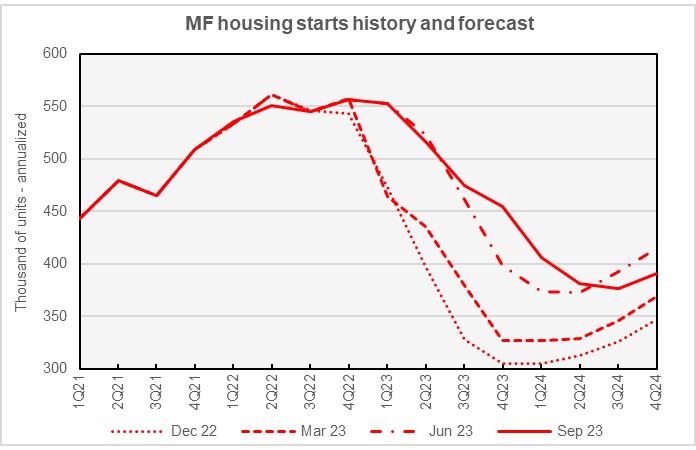

The current forecast for multifamily housing starts is shown in the first chart, below, along with three other recent forecasts. Fannie Mae considers any building containing more than one dwelling unit to be “multifamily”, including both condominiums and rental housing units.

Compared to last month’s forecast, the September forecast for multifamily starts was slightly lower for the middle of 2023, higher in the last quarter of 2023 and the first quarter of 2024 but then lower again in the last three quarters of 2024. The largest revisions for any quarter were an addition of 18,000 annualized units in Q4 2023 and a subtraction of 20,000 annualized units in Q3 2024. The lowest annualized rate of multifamily housing starts is now predicted to be 376,000 units in Q3 2024. This is 14,000 units lower than the lowest annualized starts rate predicted in last month’s forecast and the low point in starts occurs one quarter later.

Factors weighing on multifamily starts include slower rent growth, rising vacancies and tighter lending standards.

Compared to last month’s forecast, the predicted number of multifamily starts in 2023 was revised upward by 3,000 units to 499,000 units. The predicted number of multifamily starts for 2024 was revised downward by 9,000 units to 389,000 units.

Single-family starts numbers edge higher

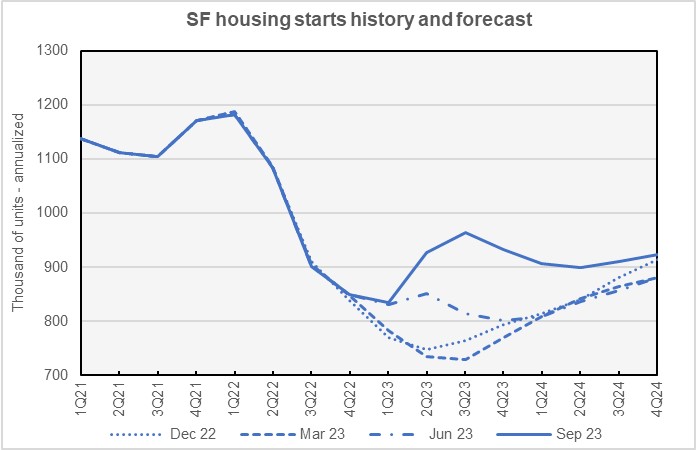

The current forecast for single-family housing starts is shown in the next chart, below, along with three other recent forecasts.

Fannie Mae’s forecasters once again raised their predicted numbers for single-family starts over almost the entire forecast horizon compared to last month’s forecast. The only quarter where the forecast number of starts was lowered was Q2 2023, the quarter just completed. The upward revisions in the other quarters were generally small with the largest revision being an addition of 7,000 annualized units in Q4 2023.

Fannie Mae now expects single-family starts to be 914,000 units in 2023, up 2,000 units from the level forecast last month. Fannie Mae now expects single-family starts to be 910,000 units in 2023, up 3,000 units from the level forecast last month.

GDP growth forecast nearly unchanged

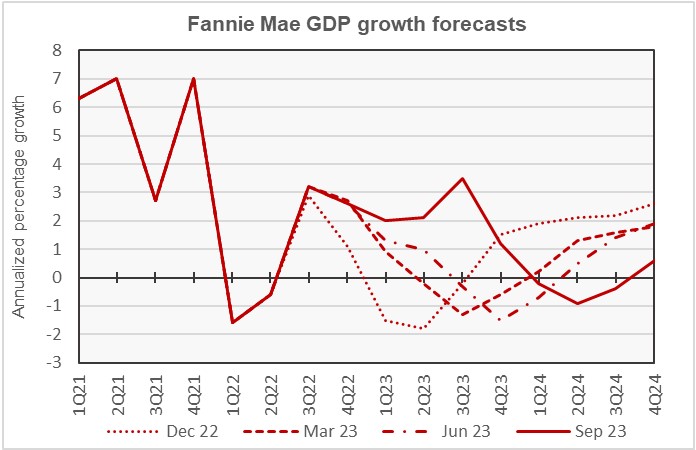

The next chart, below, shows Fannie Mae’s current forecast for Gross Domestic Product (GDP) growth, along with other recent forecasts.

Fannie Mae’s forecasters have been predicting that the economy would experience a recession since their April 2022 forecast. However, their view on the depth and timing of that recession has undergone frequent revisions. Originally forecast to start in Q3 2023, the predicted recession start date was as early as Q4 2022 in the October 2022 forecast. The current forecast puts the start of the recession in Q1 2024, with growth returning in Q4 2024.

The largest quarterly revisions in this month’s forecast were in the quarter just completed and in the current one. The year-over-year GDP growth forecast for Q2 2023 was revised downward from 2.4 percent to 2.1 percent. However, the GDP growth forecast for Q3 was revised upward from 2.2 percent to 3.5 percent.

The full year forecast for GDP growth for 2023 was revised upward by 0.3 percentage points to 2.2 percent. The full year GDP forecast for 2024 was left unchanged at -0.2 percent.

Inflation forecast nears Fed target

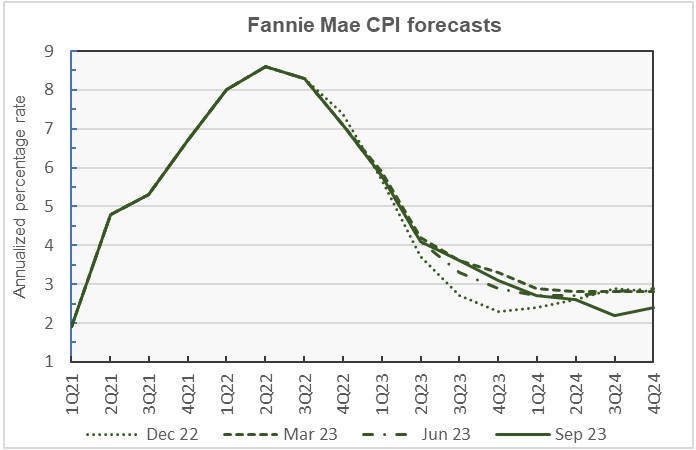

The next chart, below, shows Fannie Mae’s current forecast for the Consumer Price Index (CPI), along with three other recent forecasts.

Fannie Mae’s forecasters revised their inflation forecasts for the last two quarters of 2023 by no more than 0.1 percentage point. However, the revisions to their inflation forecasts for 2024 were larger. The largest revision was for Q3 2024 with predicted inflation being revised lower by 0.6 percentage points to 2.2 percent, year-over-year. This is only slightly above the Federal Reserve’s target of 2.0 percent inflation. However, Fannie Mae’s forecast for Q4 2024 inflation is higher, rising to 2.4 percent, so inflation is expected to move higher again at the end of the forecast window.

Looking at whole-year forecasts, the forecast for year-over-year CPI growth in Q4 2023 was revised downward from last month’s level by 0.1 percentage points to 3.1 percent, reversing last month’s revision. The Q4 2024 inflation forecast was revised downward by 0.4 percentage point to 2.4 percent.

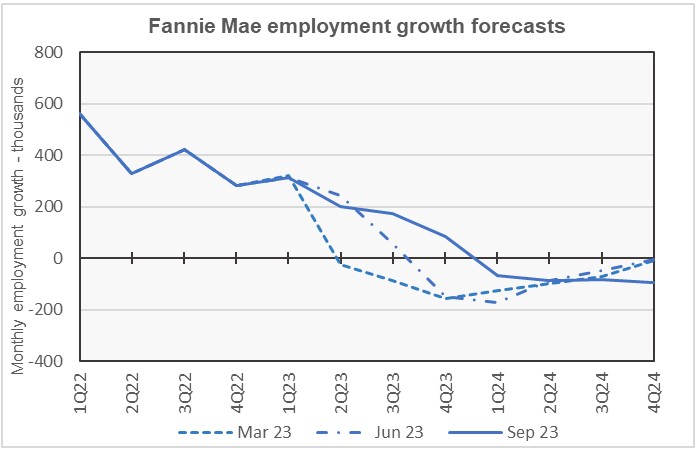

Job growth declines less rapidly

The next chart, below, shows Fannie Mae’s current forecast for employment growth, along with two earlier forecasts. Employment growth is our preferred employment metric since job gains, along with productivity gains, drive economic growth. By contrast, the unemployment rate can be lowered by lowering the labor force participation rate without achieving employment growth.

Fannie Mae revised the population base used for their employment forecasts in February 2023, so that is the earliest forecast whose employment numbers can be compared to those in the current forecast.

Fannie Mae’s forecast for job growth in 2023 reflects the recent strength of the economy, with higher forecast job growth in 2023 and slower job losses in 2024. Net job losses are expected to begin in Q1 2024, in line with last month’s forecast, but the number of jobs forecast to be lost in each quarter was reduced compared to last month’s forecast.

Compared to last month’s forecast, the full year forecast for employment growth in 2023 was revised upward from a gain of 2.0 million jobs to a gain of 2.3 million jobs. The employment growth forecast for 2024 was revised from a loss of 1.1 million jobs to a loss of 1.0 million jobs.

The Fannie Mae forecast can be found here. There are links on that page to the detailed forecasts and to the monthly commentary.