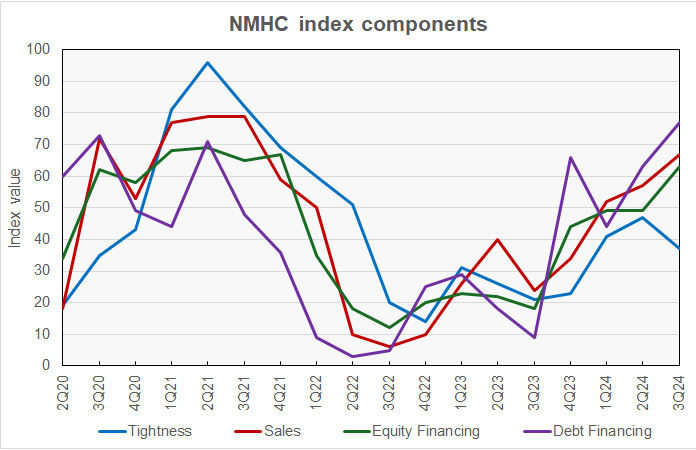

Apartment market conditions showed signs of improvement in the National Multifamily Housing Council’s (NMHC’s) October 2024 Quarterly Survey of Apartment Market Conditions. All but the Market Tightness (37) index indicated more favorable conditions this quarter, with Sales Volume (67), Equity Financing (63) and Debt Financing (77) all coming in above the breakeven level (50).

“The 10-Year Treasured yield fell 28 basis points (bps) over the past three months as the Federal Reserve enacted its first, 50 bps cut to short-term rates,” noted NMHC’s Economist and Senior Director of Research, Chris Bruen. “Survey respondents, in turn, reported more favorable conditions for debt financing for the third straight quarter and more available equity financing for the first time in two and a half years.”

“Elevated levels of multifamily deliveries, however, resulted in the ninth consecutive quarter of looser conditions, especially in the South and in Sun Belt markets. Still, strong demand for apartments has meant that much of this new supply is getting absorbed.”

- The Market Tightness Index came in at 37 this quarter – below the breakeven level of 50 – indicating looser market conditions for the ninth consecutive quarter. While close to half of respondents (46%) thought market conditions were unchanged relative to three months ago, 40% of respondents thought markets have become looser, up from 27% in July. Fifteen percent of respondents reported tighter markets than three months ago.

- The Sales Volume Index reading of 67 reflected a third straight quarter of increasing deal flow. As was the case last quarter, the plurality of respondents (46%) reported sales volume to be unchanged from three months ago. Forty-three percent of respondents reported higher sales volume this quarter, increasing from 21% of respondents in April and 32% in July, while 10% thought volume was lower.

- The Equity Financing Index flipped this quarter with a reading of 63 – the first quarter of more available equity financing since January 2022. Thirty-two percent of respondents this round reported more available equity financing, up from 13% in July, while just 6% thought it less available. Roughly half of respondents (53%) thought availability remained unchanged from three months ago.

- The Debt Financing Index also came in above the breakeven level of 50 – indicating more favorable conditions for debt financing compared to three months ago – with a reading of 77. Up from 37% in July, the majority of respondents this quarter (62%) felt now was a better time to borrow than three months ago, while 8% thought borrowing conditions were worse than three months ago. A quarter of respondents reported unchanged debt financing conditions, down from 44% last quarter.

Following an interest rate cut of 50 basis points from the Federal Reserve in September, and with the July Quarterly Survey already indicating a potential rebound in deal flow, this round of the survey firmly reflected both increasing sales volume and more favorable financing conditions. With transaction activity picking up, 38% of respondents thought that primary markets (e.g., New York, Los Angeles, Miami) were receiving an increasing share of sales volume relative to secondary and tertiary markets (e.g., Nashville, Austin, Boise). Conversely, 10% of respondents thought primary markets were receiving a decreasing share of sales activity relative to secondary and tertiary markets. The plurality of respondents (45%) viewed there to have been no relative change.

The history of the survey results is shown in the chart, below. They can also be viewed here.