The Mortgage Bankers Association (MBA) reported that multifamily mortgage debt outstanding rose by $38.88 billion in Q4 from the revised level of the quarter before. Total multifamily debt reached a level of $2.157 trillion. Compared to the year-earlier level, debt was up $111.0 billion (5.4 percent).

The growth in multifamily mortgage debt outstanding in Q4 was up 30.3 percent from the growth originally reported for Q3. However, the debt outstanding in Q3 was revised lower by $5.38 billion in the latest report.

The total of all commercial mortgage debt, including multifamily debt, outstanding at the end of Q4 rose 1.1 percent from its revised Q3 level to $4.790 trillion. Multifamily mortgage debt represented 45.0 percent of commercial mortgage debt outstanding.

Earlier, the MBA had reported that multifamily mortgage originations had risen 21.9 percent in Q4. The Q4 2024 originations index was reported to be up 68.7 percent from its level in Q4 2023.

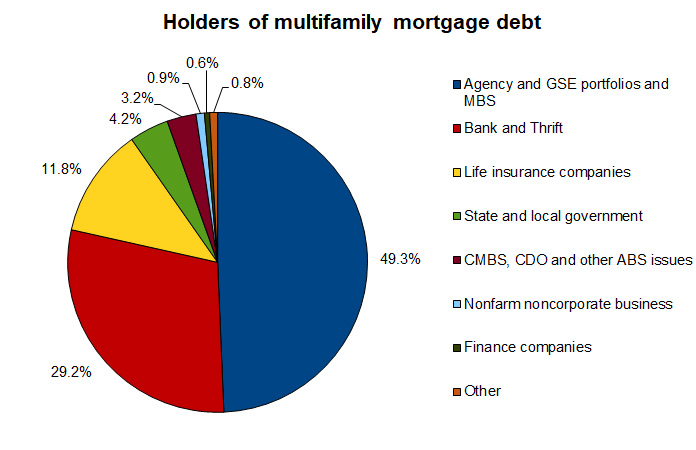

Pieces of the pie

The shares of multifamily mortgage debt held by various classes of suppliers are shown in the first chart, below.

The largest share of multifamily mortgage debt was held by “Agency and GSE portfolios and MBS”. These are agencies, like the Federal Housing Administration and Government Sponsored Enterprises (GSEs) like Fannie Mae and Freddie Mac, who buy up mortgages and sell some of the debt as Mortgage-Backed Securities (MBS). At the end of Q4, the GSEs’ holdings of multifamily debt rose 0.5 percentage points quarter-over-quarter to 49.3 percent of the total outstanding. The GSEs held $1,064 billion in multifamily debt at the end of the quarter, up $31.19 billion.

Banks and Thrifts, the second largest holders of multifamily mortgages, decreased their multifamily mortgage holdings by $837 million to $628.9 billion. Their share of outstanding debt fell 0.5 percentage points to 29.2 percent.

Life Insurance companies were reported to increase their direct holding of multifamily mortgage debt by $10.16 billion in the quarter. They held $254.5 billion in mortgages at the end of the quarter. Their share of total multifamily debt outstanding rose 0.3 percentage points from the revised level of the quarter before to 11.8 percent. However, this figure does not account for the multifamily mortgages these companies hold through commercial mortgage-backed securities (CMBS).

State and local governments held 4.2 percent of outstanding multifamily mortgage debt at the end of Q4, down 0.2 percentage points from the revised level reported for the previous quarter. They decreased their holdings by $1.62 billion to a total of $91.65 billion at the end of the quarter.

CMBS, CDO (collateralized debt obligations) and other ABS (asset backed securities) issuers increased their holdings of multifamily mortgage debt in Q4 by $282 million to $68.06 billion. Their share of mortgage debt outstanding was unchanged at 3.2 percent.

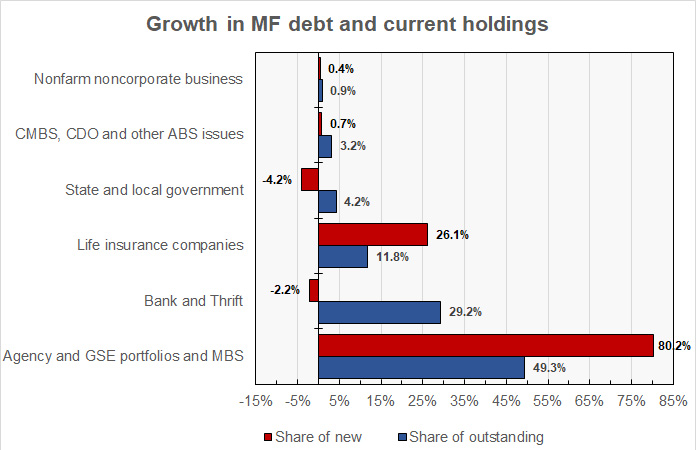

Who’s growing?

The next chart, below, plots the current share of multifamily mortgage debt outstanding for a given class of lender alongside that class of lender’s share of net new mortgage debt outstanding in Q1. When the latter share is greater than the former, that class of lender is increasing its share of the multifamily mortgage market.

The chart shows that the GSEs accounted for by far the largest share of the net increase in multifamily mortgage debt outstanding, well above their share of current holdings. Of the net increase in multifamily debt outstanding in the quarter, 80.2 percent came from the GSEs.

Banks and thrifts shrunk their holdings of multifamily mortgage debt, accounting for a 2.2 percent decrease in the total multifamily debt outstanding. This is why their share of holdings of total multifamily debt outstanding fell.

Life insurance companies again grew their holdings of multifamily mortgage debt at a rate more than twice their share of multifamily mortgage debt outstanding. Their increase in holdings of multifamily debt represented 26.1 percent of the quarterly increase and 25.5 percent of the annual increase in total multifamily debt outstanding.

State and local governments decreased their holdings of multifamily debt for the second consecutive quarter. Their decrease in holdings was the largest on a percentage basis and also in net dollars of any of the lender types covered in the report.

The shares of the growth in multifamily mortgage debt outstanding of the other lender types in the top 6 were less than their shares of existing mortgage debt, although they did not actually reduce their holdings. However, they are continuing to become relatively less important as sources of funds.

The report does not cover loans for acquisition, development or construction, or loans collateralized by owner-occupied commercial properties. The full report also includes information on mortgage debt outstanding for other commercial property types. The full report can be found here.