CoStar reported that its value-weighted index of multifamily property prices fell month-over-month in July, dropping 1.36 percent. This index was up 3.11 percent year-over-year.

By contrast, MSCI Real Capital Analytics reported that multifamily property prices were unchanged for the month and up 0.4 percent year-over-year in July.

The value-weighted index of non-multifamily commercial property rose 1.37 percent month-over-month in July. This index is down 3.91 percent year-over-year. The other commercial property types tracked by CoStar are office, retail, industrial and hospitality.

For more information on the CoStar Commercial Repeat Sales Indexes (CCRSI’s), please see the description at the bottom of this report.

Multifamily property prices turn lower

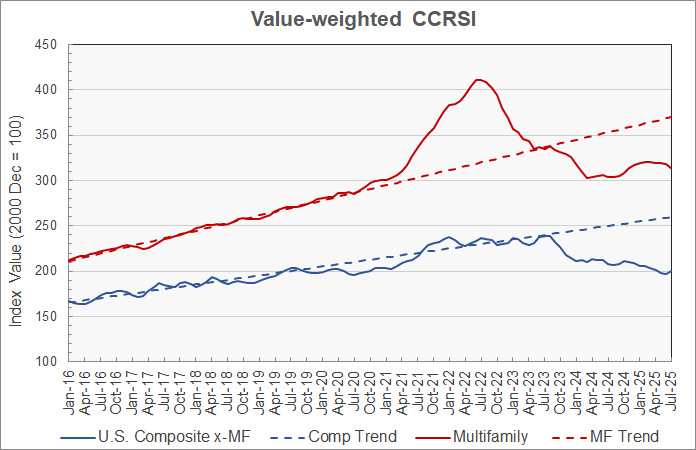

The first chart, below, shows the history of the value-weighted CCRSI’s since January 2016 for multifamily property and for all other commercial property considered as a single asset class. It also shows trend lines for the growth in the two CCRSI’s based on their growth in the period from January 2012 to January 2020. The indexes are normalized so that their values in December 2000 are set to 100.

The chart shows that multifamily property prices trended higher between March 2024 and February 2025. However, since then property prices have been declining slowly. Multifamily property prices are down 23.8 percent from their all-time high. They are 15.3 percent below their pre-pandemic trend.

Prices for other commercial property types rose this month after declining for the 4 previous months. These prices are now 16.4 percent below their high point and 23.1 percent below their pre-pandemic trend.

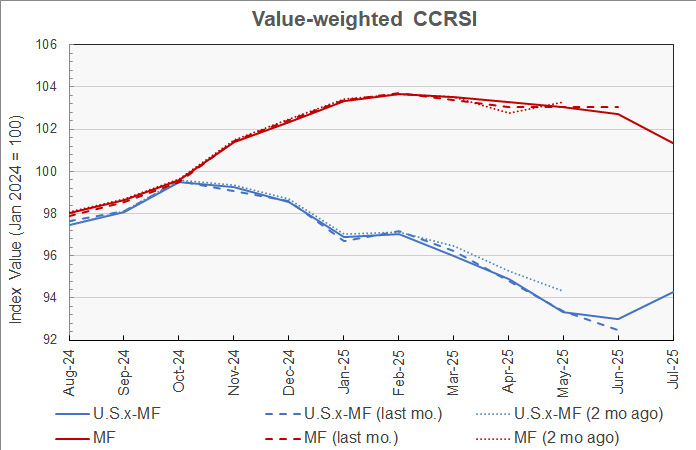

The second chart shows the recent history of multifamily property prices and other commercial property prices based on this month’s data along with the estimates from last two month’s reports. For purposes of this chart, the price indexes for both property groupings were each set to a value of 100 in January 2020 relative to the price indexes for that date in the current report. This allows the indexes to be plotted together at a scale that shows the detailed price movements.

The chart shows that new transactions added to the multifamily data set did not make a significant difference in the reported price level, but they did affect the apparent direction of the price movement. For example, the original report for May indicated that multifamily property prices were up 0.5 percent for the month. The next month’s report indicated that prices were flat in May, and the current report indicates that prices fell 0.2 percent in May.

This month’s revisions to the non-multifamily property price data indicate that prices were lower in May than originally reported but they were higher in June than originally reported.

Transaction volumes higher compared to initial report

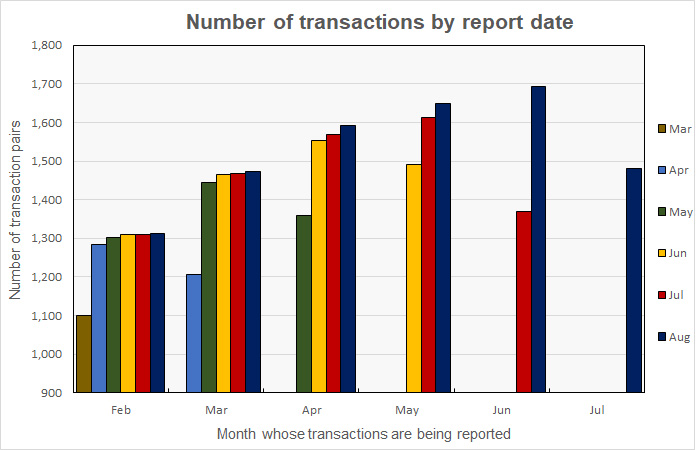

An issue with monthly transaction volume reporting is that CoStar usually identifies additional transactions to tabulate over the next few months after the initial report, and these extra transactions tend to make initial reports of falling transaction volumes appear more negative than they will subsequently appear. For example, CoStar reported that the transaction volume in July for all property types was down 212 transactions (12.5 percent) from the revised level of the month before. However, it was up 112 transactions (8.2 percent) from the preliminary level for June reported last month.

CoStar reported that their initial transaction count for July was 1,482 repeat sales pairs. This is up from the 1,370 transaction pairs identified for June in last month’s report but down from the 1,694 transaction pairs identified for June in this month’s report.

The history of the revisions to the transaction counts for recent months is illustrated in the next chart. It shows that the number of transactions for February was initially given as 1,101 in the March report and has been updated in every subsequent report. While the size of the transaction count revision was largest in the next month’s report, additional transaction pairs for February continued to be identified in every subsequent report. The current report identifies 1,312 transactions for February. By contrast, transaction data for July only appears in the current (August) report and we can expect it to be revised next month.

The preliminary dollar volume of transactions was reported to fall 4.4 percent from the revised level of the month before to $10.70 billion. However, the dollar volume of transactions increased 9.5 percent from the preliminary level reported last month.

Distress levels roughly stable

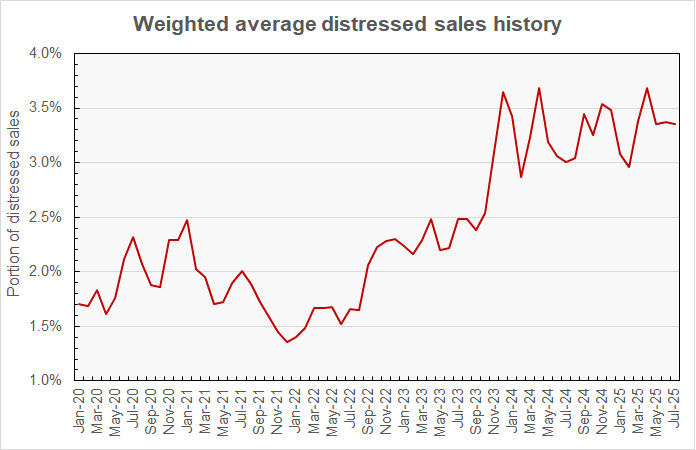

CoStar also reported on the portion of sales that would be considered “distressed”. The next chart shows the distressed sales trends for combined investment grade and commercial grade property sales. Multifamily distressed sales are not separated out from those of other property types in this data. Because of volatility in the data, the chart presents the 3-month weighted moving average of CoStar’s distressed sales data.

The chart shows that the portion of sales that CoStar designates as distressed seem to have reached a plateau, if a bumpy one, since late 2023. Since November 2023, distressed sales have averaged 3.4 percent of sales.

The full report discusses all commercial property types. While the CoStar report provides information on transaction volumes, it does not break out multifamily transactions. The latest CoStar report can be found here.

CCRSI defined

The CoStar report focuses on a relative measure of property prices called the CoStar Commercial Repeat Sales Index (CCRSI). The index is computed based on the resale of properties whose earlier sales prices and sales dates are known. The index represents the relative change in the price of property over time rather than its absolute price. CoStar identified 1,482 repeat sale pairs in July for all property types. These sales pairs were used to calculate the results quoted here.

CoStar computes CCRSI’s for a variety of property groupings, combining them by cost, region, property type or other factors. The value-weighted index is more heavily influenced by transactions of expensive properties than is CoStar’s equal-weighted index. The value-weighted index is the focus of this report because it is an index whose value is reported monthly and for which CoStar breaks out multifamily property as a separate category.