Revisions to Fannie Mae’s September housing forecast raise the number of multifamily starts expected in 2025 and 2026 from those in last month’s forecast. Fannie Mae is now predicting 412,000 starts in 2025 with 402,000 starts in 2026. The outlook for single-family housing starts is more mixed with slightly more starts predicted for 2025 and slightly fewer starts predicted for 2026 than in last month’s forecast.

Interest rate outlook lowered

Fannie Mae’s forecasters lowered their predicted trajectory of the Fed Funds rate in this forecast. They predict the average Fed Funds rate in Q4 2025 will be 3.8 percent. This is down from their prediction of 4.0 percent last month and down from its level of 4.3 percent in Q3. They predict the average Fed Funds rate for Q4 2026 will be 3.1 percent, down from last month’s prediction of 3.4 percent.

The forecast for the for the 10-year Treasury rate was also lowered, but only slightly. The forecasters reduced their predicted interest rate in Q4 2025 by 0.1 percentage points to 4.3 percent. They also lowered their predicted rate in Q4 2026 by 0.1 percentage points to 4.4 percent. These are the same rates they were predicting in their July forecast.

Multifamily starts forecast raised

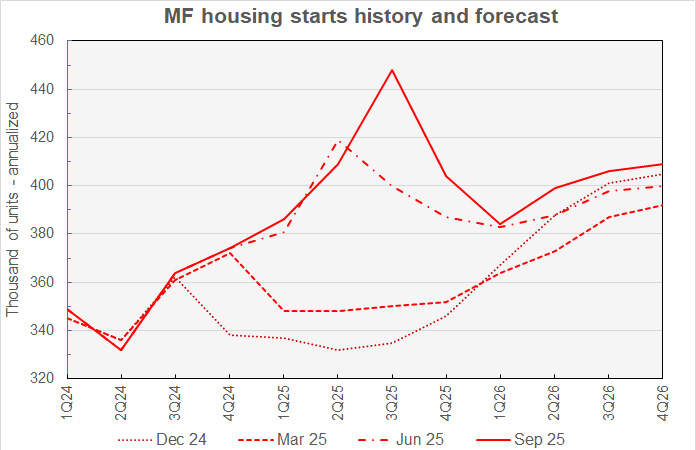

The current forecast for multifamily housing starts is shown in the first chart, below, along with three other forecasts from the last year. Fannie Mae considers any building containing more than one dwelling unit to be “multifamily”, including both condominiums and rental housing units.

For the second month in a row and the seventh time in the last 8 forecasts, Fannie Mae’s forecasters raised their predicted level of multifamily starts in 2025. They are now expecting 412,000 unit starts, up from 389,000 predicted last month and from only 319,000 predicted in January.

The largest quarterly revision this month was to the current quarter. The Q3 estimate was revised 59,000 annualized units higher to 448,000 annualized units. For reference, the latest report from the Census Bureau has multifamily starts running at an annualized rate of 444,000 units in Q3, although these results are preliminary.

Q3 2025 is now predicted to be the cycle high for multifamily starts. Starts are then predicted to fall to a low of 386,000 annualized units in Q1 2026 before beginning a new upward trend. However, multifamily starts are only forecast to recover to a level of 409,000 annualized units by the end of 2026.

Looking at yearly forecasts, the predicted number of multifamily starts for 2025 was revised higher by 23,000 units. The forecast for multifamily starts in 2026 was revised higher by 10,000 units.

Revisions mixed for single-family starts

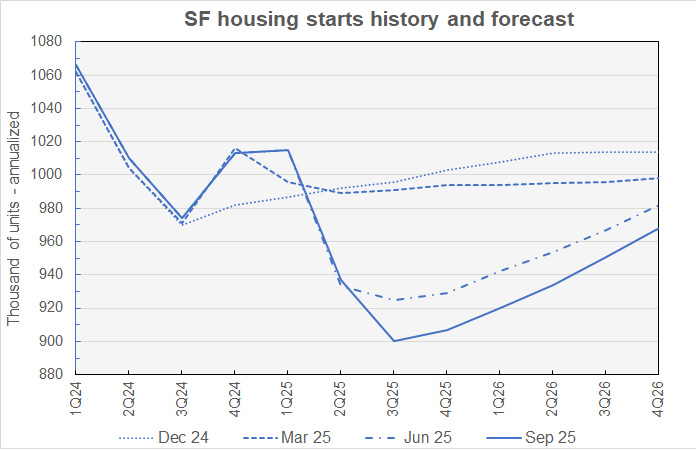

The current forecast for single-family housing starts is shown in the next chart, below, along with three other recent forecasts.

After downward revisions to all quarterly forecasts last month, the single-family starts quarterly forecasts for 2025 were all revised higher this month. The largest quarterly revision made was to the Q2 2025 “forecast”, which was raised by 18,000 annualized units to 937,000 annualized units. The revisions made to the successive quarterly forecasts were progressively smaller, with the Q1 2026 forecast being unchanged. The remaining quarterly forecasts for 2026 were lowered, but none by more than 7,000 annualized units.

The low point for single-family starts going forward is again predicted to be Q3 2025 with 900,000 annualized unit starts. Starts are forecast to rise from that point and are predicted to reach an annualized rate of 968,000 units in Q4 2026.

For reference, the Census Bureau’s new residential construction report for August put Q2 2025 single-family starts at 941,000 annualized units. The Q3 figure, based on the preliminary data from the first two months of the quarter, was 924,000 annualized starts.

Looking at full-year predictions, Fannie Mae now expects 9,000 more single-family starts in 2025 than forecast last month at 940,000 units. Fannie Mae now also expects 5,000 fewer single-family starts in 2026 than forecast last month at 943,000 units.

Near-term GDP growth forecasts higher

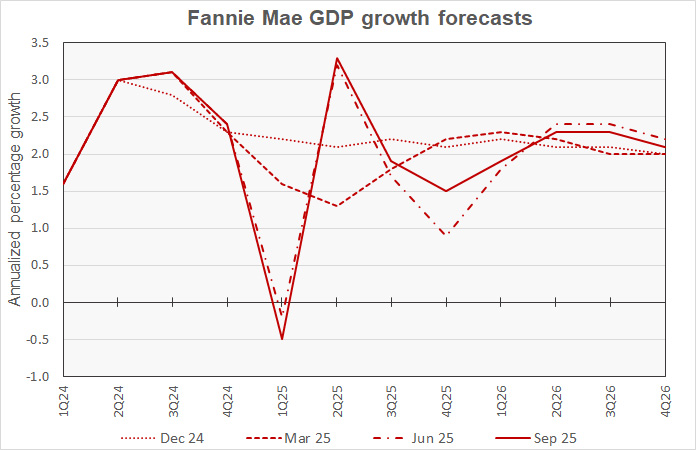

The next chart, below, shows Fannie Mae’s current forecast for Gross Domestic Product (GDP) growth, along with other recent forecasts.

The estimate for Q2 2025 GDP growth was again revised higher this month, rising 0.3 percentage points to 3.3 percent. This is in line with the Bureau of Economic Analysis’ second estimate.

After being revised sharply lower last month, the Q3 2025 forecast was revised sharply higher this month, rising 1.3 percentage points to 1.9 percent. The Q3 GDP growth estimate had been 1.7 percent in July’s forecast, but only 0.6 percent in last month’s forecast. The forecast for Q1 2026 was raised 0.2 percentage points but other quarterly forecasts for 2026 were lowered.

Fannie Mae’s forecasters now expect year-over-year GDP growth to be 1.5 percent in 2025, up 0.4 percentage points from the rate predicted last month. They expect 2.1 percent GDP growth in 2026, down 0.1 percentage point from their last prediction.

For reference, the September 17 release of the GDP Now estimate from the Atlanta Fed indicates that Q3 2025 annualized GDP growth is currently running at 3.3 percent. This is well above their “blue chip consensus” Q3 forecast, which is currently around 1.2 percent.

PCE Inflation forecasts lower

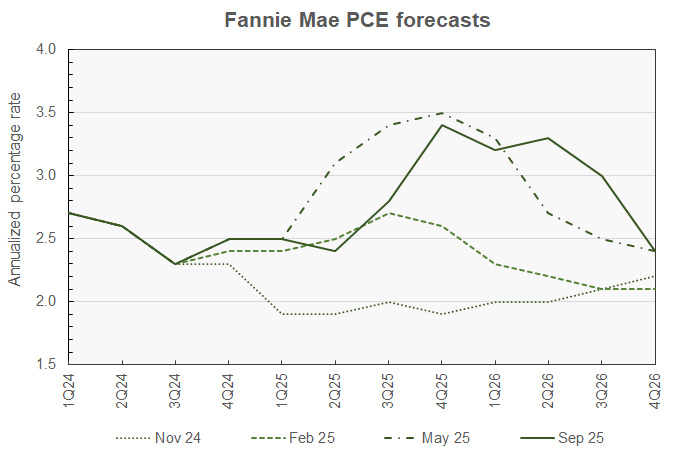

The next chart, below, shows Fannie Mae’s current forecast for the chained personal consumption expenditures (PCE) inflation rate, along with three other recent forecasts.

Fannie Mae’s forecasters revised their PCE inflation estimates higher last month but nearly reversed most of those revisions this month. Inflation estimates for Q3 2025 through Q2 2026 were each revised lower by either 0.3 or 0.4 percentage points.

Fannie Mae’s prediction for the year-over-year inflation rate for Q4 2025 was revised 0.3 percentage points lower to 3.4 percent. Their predicted for the year-over-year inflation rate for Q4 2026 was left unchanged at 2.4 percentage.

For reference, the Bureau of Economic Analysis estimated that PCE inflation was running at 2.6 percent in July 2025.

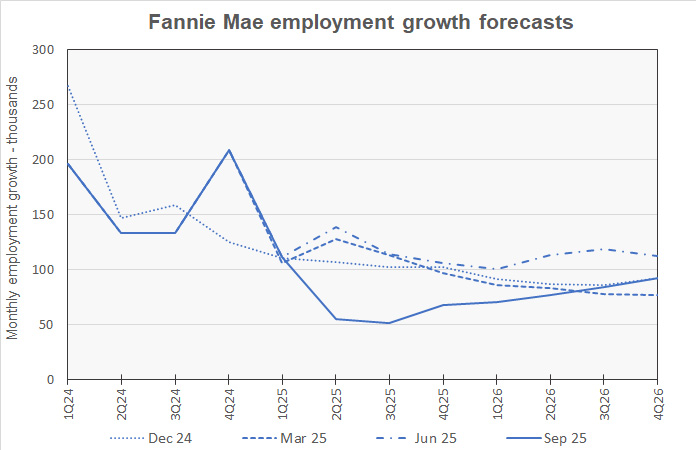

Employment growth forecast lower

The next chart, below, shows Fannie Mae’s current forecast for employment growth, along with three earlier forecasts. Employment growth is our preferred employment metric since job gains, along with productivity gains, drive economic growth. By contrast, the unemployment rate depends on employment but also on the labor force participation rate. Either rising employment or falling labor force participation can drive the unemployment rate lower, but only the former would contribute to economic growth.

In the wake of the Bureau of Labor Statistics making sharp downward revisions to their employment growth estimates, Fannie Mae’s forecasters reduced their employment growth estimates again this month.

The largest revision to the employment growth estimates was for Q3 2025, which was revised lower by 37,000 jobs per month to only 51,000 jobs per month. While all subsequent quarterly employment growth forecasts were also revised lower, no other revision exceeded 18,000 jobs per month.

Employment growth in 2025 is now expected to be 900,000 jobs, down 100,000 jobs from last month’s prediction. Employment growth for 2026 is expected to be 1,000,000 jobs, also down 100,000 jobs from last month’s predicted level.

The Fannie Mae September forecast can be found here. There are links on that page to the detailed economic and housing forecasts.