Fannie Mae’s September housing forecast calls for fewer multifamily housing starts in 2024 and 2025 than in last month’s forecast. The downward revision follows two monthly forecasts where the predictions for multifamily starts were revised higher.

The forecast for single-family housing starts was also revised lower through the end of 2025. Starts are still expected to trend downward through Q3 2024 and then to rise through the end of 2025.

Fannie Mae’s forecast was issued before the conclusion of the meeting of the Federal Reserve’s Federal Open Market Committee (FOMC) and Fannie Mae’s interest rate forecasts deviate significantly from those of the Fed. Specifically, the FOMC projects the Fed Funds rate to end 2024 at 4.1 percent while Fannie Mae’s forecasters expected the rate to be 4.9 percent. The FOMC now projects the Fed Funds rate to end 2025 at 3.4 percent while Fannie Mae’s forecasters expected the rate to only fall to 3.7 percent.

The 10-year Treasury was reported to be at 4.4 percent in Q2 2024. It is now predicted to drop to 4.0 percent in Q3 and 3.9 percent in Q4 2024. It is forecast to also end the year 2025 at that level. This rate is about a quarter point lower than the rate predicted in last month’s outlook.

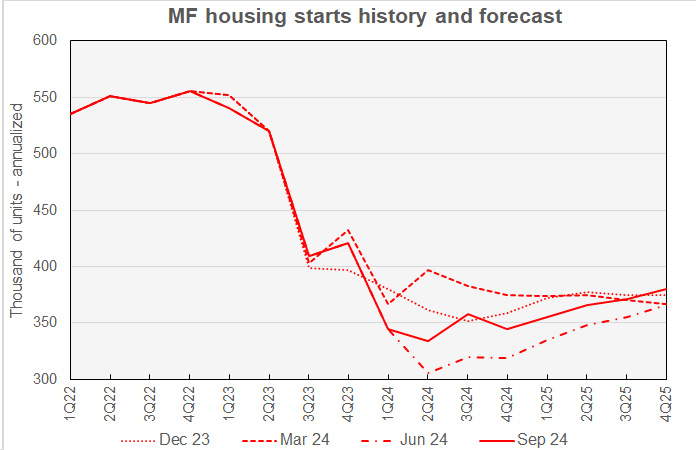

Multifamily starts forecast lower

The current forecast for multifamily housing starts is shown in the first chart, below, along with three other recent forecasts. Fannie Mae considers any building containing more than one dwelling unit to be “multifamily”, including both condominiums and rental housing units.

Fannie Mae’s forecasters revised their multifamily housing starts forecasts lower this month over their entire forecast horizon, with the exception of a small upward revision to the forecast for Q3 2024. The low point for multifamily starts is still seen as being in Q2 2024, but the forecast number of starts for that quarter was lowered by 8,000 annualized units to 334,000 annualized units.

For reference, the most recent new residential construction report from the Census Bureau has multifamily starts running at a seasonally-adjusted annualized rate of 336,000 units in Q2 and 372,000 units through the first two months of Q3 2024. However, revisions to the Q3 data are likely.

Fannie Mae’s current forecast calls for multifamily starts to trend higher starting in Q3 2024, continuing through the end of 2025. Starts are predicted to finish 2025 at a rate of 380,000 annualized units. This is 23,000 annualized units lower than in last month’s forecast.

Looking at yearly forecasts, the predicted number of multifamily starts for 2024 was revised lower by 4,000 units to 345,000 units. The forecast for multifamily starts in 2025 was revised lower by 22,000 units to 368,000 units.

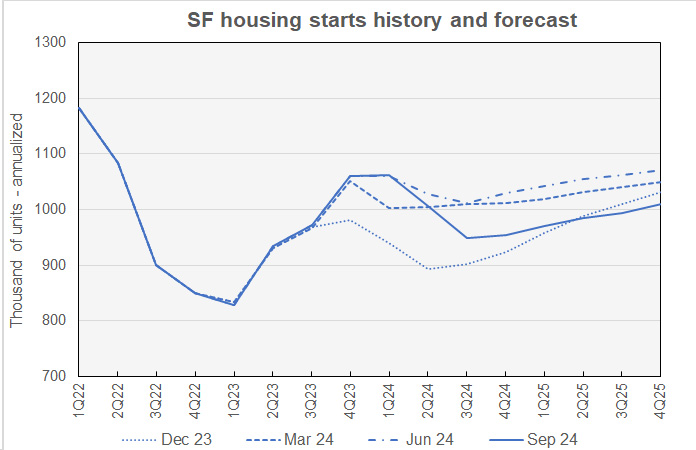

Single-family starts forecast revised lower again

The current forecast for single-family housing starts is shown in the next chart, below, along with three other recent forecasts.

Every single-family starts forecast since April has predicted lower numbers of starts. In the current forecast, each quarterly prediction for single-family starts from Q3 2024 through the end of 2025 was lower than in last month’s forecast. The Q3 2024 forecast was revised lower by 22,000 annualized units and is now 94,000 units lower than predicted in April. The forecasts for the following quarters were also revised lower with the largest revision being a 24,000 annualized unit downgrade for Q4 2025.

The low point for single-family starts is now expected to be in Q3 2024. The annualized number of single-family starts expected in that quarter is 948,000. Single-family starts are then forecast to rise gradually, reaching 1,009,000 annualized units in Q4 2025.

Looking at their full-year predictions, Fannie Mae now expects single-family starts to be 993,000 units in 2024, down 8,000 units from the level forecast last month. Single-family starts in 2025 are forecast to be 989,000 units, down 17,000 units from the level forecast last month.

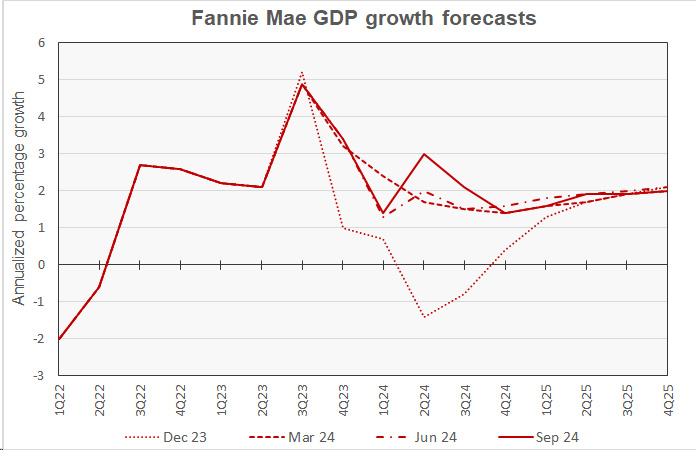

GDP growth outlook revised higher for 2024

The next chart, below, shows Fannie Mae’s current forecast for Gross Domestic Product (GDP) growth, along with other recent forecasts.

The September forecast for Q2 2024 GDP growth was revised higher again this month, rising 0.2 percentage points to 3.0 percent at a seasonally adjusted annualized rate. This is in line with the second estimate for Q2 GDP from the Bureau of Economic Analysis. The other revisions made by Fannie Mae’s forecasters were a mix of upward and downward adjustments with no individual revision greater than 0.2 percentage points.

The low point in the annualized rate of GDP growth is now expected to be in Q4 2024, with a rate of 1.4 percent. The annualized rate of GDP growth is predicted to climb over 2025, but only reach a rate of 2.0 percent by Q4.

The full year forecast for GDP growth for 2024 was raised 0.1 percentage points to 2.0 percent while the full-year forecast for 2025 was unchanged at 1.8 percent.

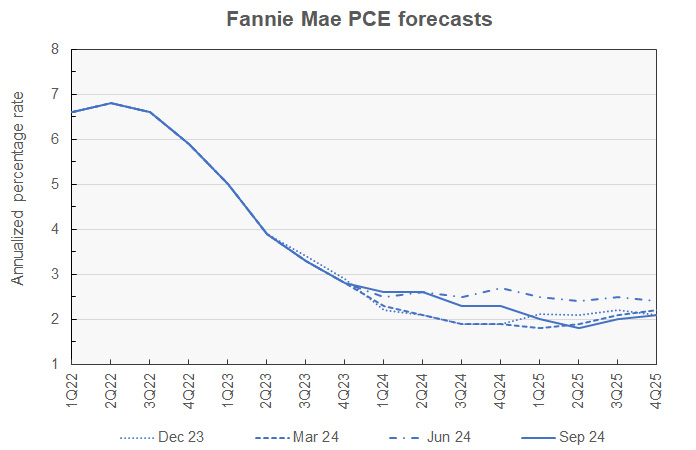

Lower PCE Inflation predicted

The next chart, below, shows Fannie Mae’s current forecast for the chained personal consumption expenditures (PCE) inflation rate, along with three other recent forecasts. We are using this index rather than the CPI this month to allow more direct comparison to the data in the Federal Reserve’s forecast.

The revisions to Fannie Mae’s PCE inflation quarterly forecasts were all to the downside this month. Inflation was predicted to be 0.1 percentage point lower in Q3 2024 and Q1 and Q3 2025. It was predicted to be 0.2 percentage points lower in Q4 2024 and Q2 2025. The predicted inflation rate in Q4 2025 was unchanged from last month’s forecast.

Looking at whole-year forecasts, the predicted year-over-year CPI inflation rate in Q4 2024 was lowered 0.2 percentage points to 2.3 percent. The Q4 2025 year-over-year inflation forecast was lowered 0.3 percentage points to 2.1 percent.

Despite these forecast inflation rates being lower than those predicted by the Fed, Fannie Mae’s forecasters did not expect that the Fed would embark on as aggressive an interest rate cutting program as they seem to have launched.

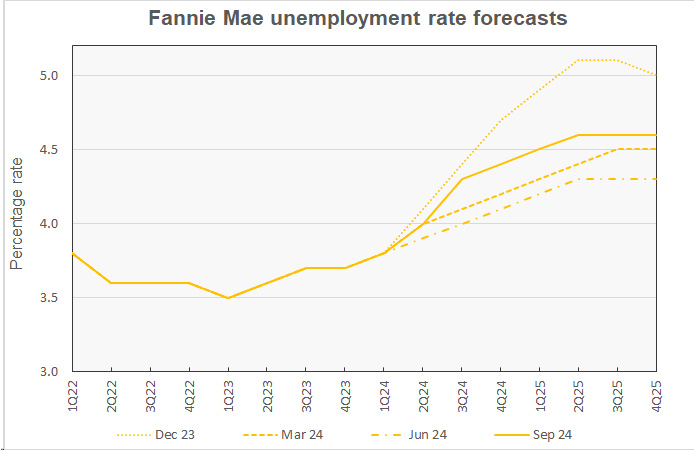

Unemployment slated to rise

To allow easier comparison to the data in the Federal Reserve’s economic projections, this month we will look at the unemployment rate rather than the employment level. Fannie Mae’s current unemployment rate forecast is show in the next chart along with three other earlier forecasts.

While there are differences between the current forecast and the other forecasts shown in the chart, there were no changes in the September unemployment rate forecast from that of the month before. The unemployment rate is predicted to climb from 4.0 percent in Q2 2024 to 4.6 percent in Q2 2025 and then stay there for the rest of the year.

For reference, the household survey in the Employment Situation Report from the Bureau of Labor Statistics said that the unemployment rate was 4.1 percent in June 2024, the end of Q2.

The forecast for the year-end unemployment rate in 2024 is 4.1 percent. The forecast for the year-end unemployment rate in 2025 is 4.6 percent. The Fed predicts unemployment rates of 4.4 percent for both periods.

The Fannie Mae September forecast can be found here. There are links on that page to the detailed forecasts and to the monthly commentary.