Size and location are factors when it comes to student housing property performance, according to the 2024 Fall report and podcast by Yardi Matrix on November 21.

Yardi Matrix expects another great year for student housing with preleasing on par with the last two years, but with slower rent growth particularly in markets with high supply, both on- and off-campus and traditional multifamily. The decline in new student housing deliveries is expected to be a tailwind in the midterm.

Preleasing and rent growth got off to a strong start, but slowed in the spring. Occupancy ended at 93.9 percent, down from last year, with over 20 percent of Yardi markets reaching 99 percent plus occupancy. Rent growth throughout the leasing season averaged six percent, down from 6.6 percent last year, but still above the average of 2.6 percent since 2018.

Early preleasing data for 2025 suggests another strong start, with 25 percent of properties reporting an average of 22.8 percent pre-leased.

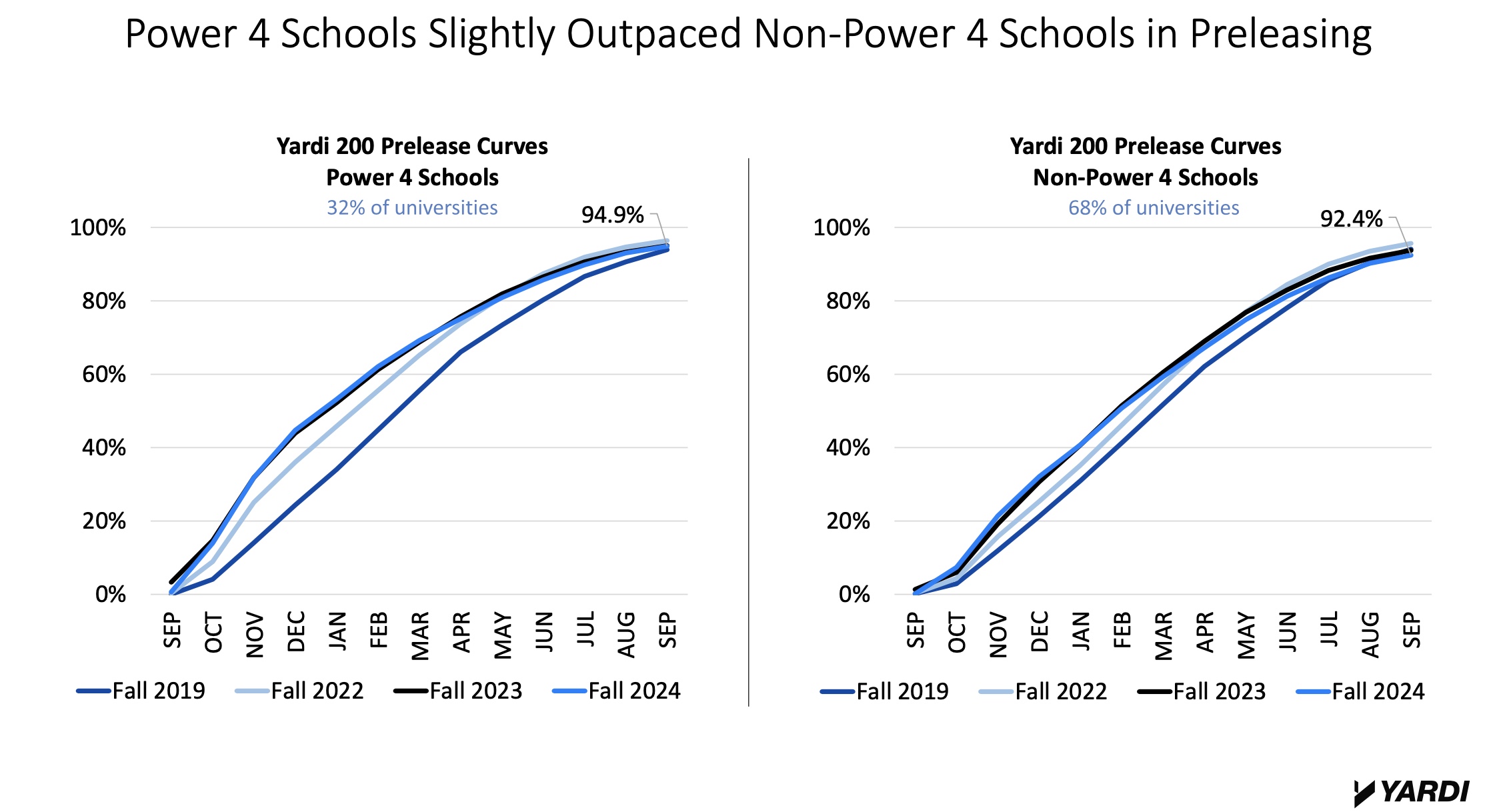

Preleasing and occupancy performance were strongest among the Power Four and primary state schools. Over the past six years, rent growth at Power Four schools has far outpaced non-Power Four schools, leading to strong investor preference for these markets.

Size and location matter

Size and location matter

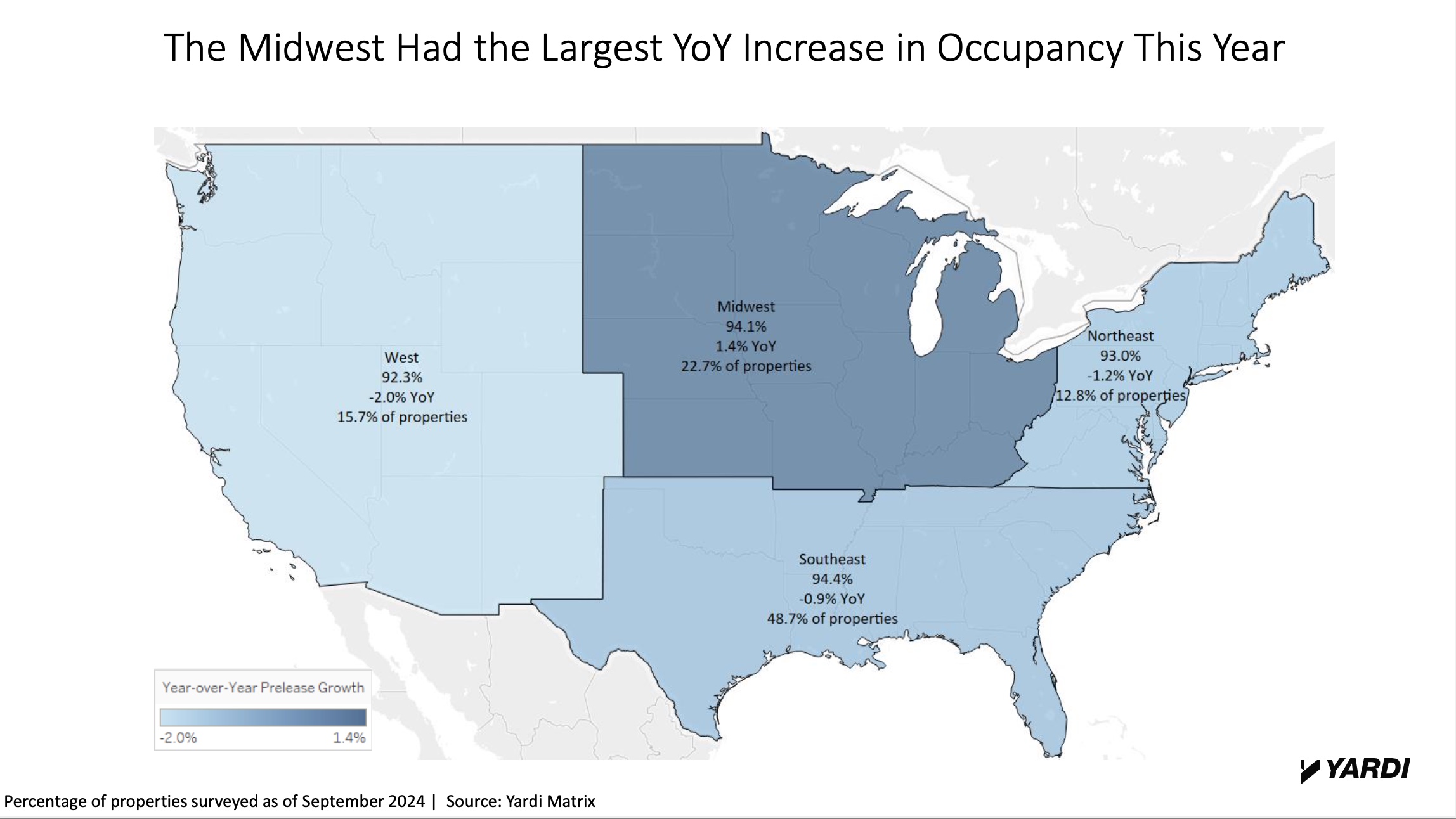

Occupancy and performance varied by region, with the Midwest and Southeast outperforming and the Northeast and West underperforming in 2024. The Midwest saw occupancy increase, while the Northeast struggled with weaker demand. See chart below.

School size and selectivity also impacted preleasing and occupancy, with larger and more selective schools performing better. Schools with more than 30,000 students outperformed their peers on preleasing and occupancy, reaching 94.8 percent occupancy in Fall 2024 versus less than 93 percent occupancy at schools with less than 30,000 students.

Because primary state schools tend to be larger and better off financially, they can offer students more academic programs and amenities, including better on and off-campus student housing, notes the report.

Rent growth has also been higher at the largest state schools, hitting 7.7 percent during the fall leasing season in 2023, and seven percent during the 2024 leasing season. Rents also grew at schools with enrollment under 15,000, but only 4.7 percent, after experiencing declining rents in 2020 through 2022.

More selective schools saw higher enrollment, occupancy and rent growth in recent years than schools accepting a higher percentage of applicants.

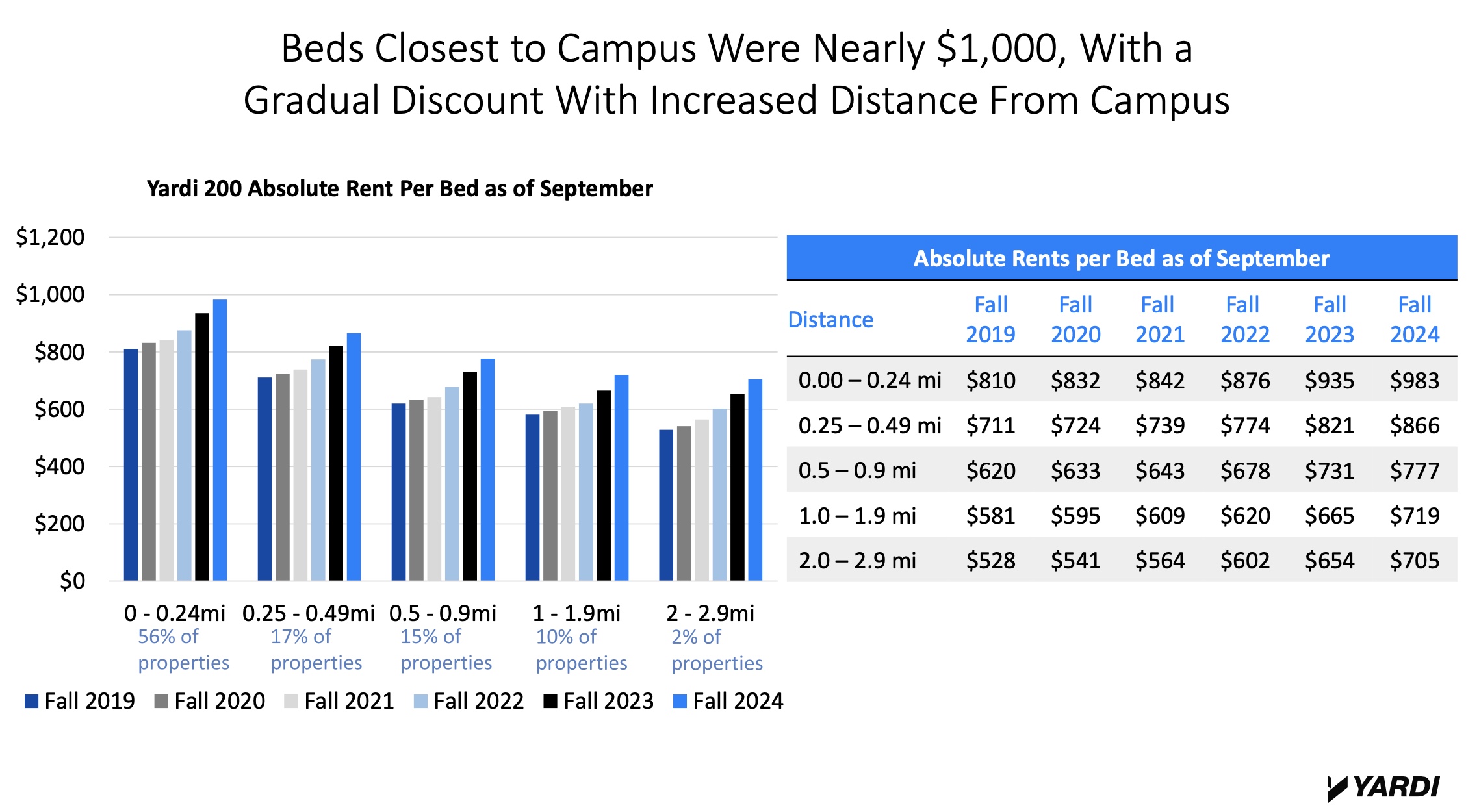

Properties close to campus have historically preleased faster and achieved higher occupancy rates, but may be starting to become victims of their success. Properties under a quarter mile from campus outperformed from 2019 through fall 2022, but recent preleasing performance has been more even across different groupings. Most of the new supply built in recent years has been less than half a mile from campus, creating more competition amongst that supply set, which makes up 58 percent of the Yardi 200 properties surveyed.

Rents are still much higher for properties next to campus, approaching $1,000 per bed in 2024, while properties further from campus typically offer more affordable rents and rent growth was still greater among properties furthest from campus.

Another differentiating factor, besides size and location by region, is urban versus rural and small-town markets. Urban markets like Georgia Tech tend to have more properties next to campus, while rural and small-town markets like Georgia Southern have more properties further from campus.

Another differentiating factor, besides size and location by region, is urban versus rural and small-town markets. Urban markets like Georgia Tech tend to have more properties next to campus, while rural and small-town markets like Georgia Southern have more properties further from campus.

Performance has varied across property types. For the second consecutive year, cottage-style properties, a newer product type, outperformed garden and mid- to high-rise properties on occupancy. But Yardi noted a much wider variance in occupancy performance with college properties posting higher occupancy this year than last.

Rent growth has been slightly more mixed among the property types, with garden-style buildings seeing the highest rent growth. But, similar to college and urban cottage-style properties, rents per bed are higher for urban assets. Interestingly, rents per bed at college properties surpassed garden-style products for the first time this year.

The entire podcast is available here.