Fannie Mae’s January economic forecast is their first since April 2022 that does not anticipate that the U.S. economy will go into recession as the Federal Reserve works to bring inflation under control. The housing forecast predicts that multifamily starts will be higher in 2024 but lower in 2025 than they predicted last month.

Multifamily starts will slowly decline

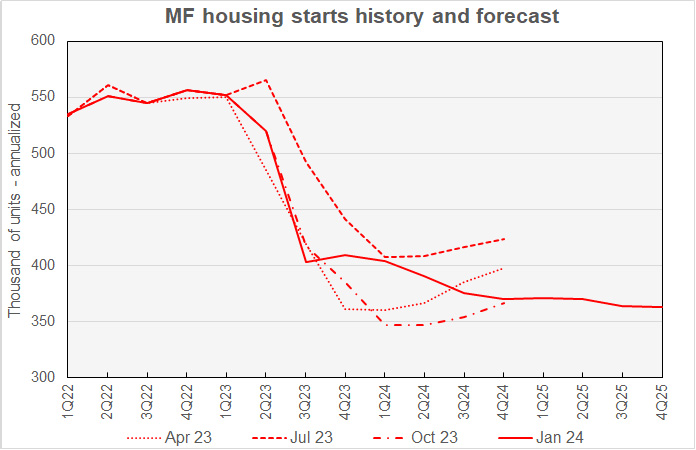

The current forecast for multifamily housing starts is shown in the first chart, below, along with three other recent forecasts. Fannie Mae considers any building containing more than one dwelling unit to be “multifamily”, including both condominiums and rental housing units.

The latest forecast revises the quarterly multifamily starts numbers to indicate that starts finished 2023 stronger than Fannie Mae had anticipated last month and that they will remain higher through 2024. While last month’s forecast predicted that multifamily starts would decline through Q3 2024 and then increase again, the current forecast has starts declining continuously through the end of 2025. However, the minimum level that starts are predicted to reach in this month’s forecast is higher than the minimum predicted last month.

The largest modification from last month’s forecast was a call for 29,000 (annualized) additional multifamily starts in Q2 2024. The starts level in Q3 2024, the low point in last month’s forecast, was revised higher by 23,000 annualized units in this month’s forecast.

The changes to the multifamily starts forecasts are in response to the perception that the Federal Reserve switched to a less hawkish stance after its December meeting. Fannie Mae’s forecasters are predicting that the Fed Funds rate will peak in Q1 2024 and that the Fed will cut the rate by a total of 100 basis points by the end of 2024.

Looking at yearly forecasts, the predicted number of multifamily starts in 2023 was revised higher by 4,000 units to 471,000 units. The predicted number of multifamily starts for 2024 was revised higher by 22,000 units to 385,000 units. The forecast for multifamily starts in 2025 was revised lower by 8,000 units to 367,000 units.

Note that the July 2023 forecast, which appears in the above chart, was the highest level ever predicted for multifamily starts by Fannie Mae.

Single-family starts seen rising

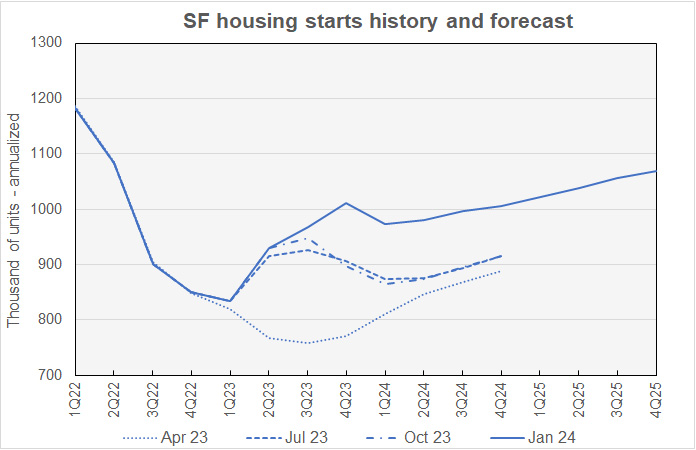

The current forecast for single-family housing starts is shown in the next chart, below, along with three other recent forecasts.

Compared to last month’s forecast, Fannie Mae’s forecasters again raised their single-family starts forecasts for every quarter of their forecast horizon. They continue to expect a pullback in single-family starts in Q1 2024 but starts will increase after that time.

Fannie Mae revised their forecast for Q1 2024 higher by 34,000 annualized units. The largest revision to starts by quarter was an upward revision of 94,000 annualized units in Q3 2024.

Fannie Mae now expects single-family starts to be 935,000 units in 2023, up 7,000 units from the level forecast last month. Fannie Mae now expects single-family starts to be 989,000 units in 2024, up 75,000 units from the level forecast last month. Single-family starts in 2025 are forecast to be 1,046,000 units, up 49,000 units from the level forecast last month.

Only slow GDP growth expected in 2024

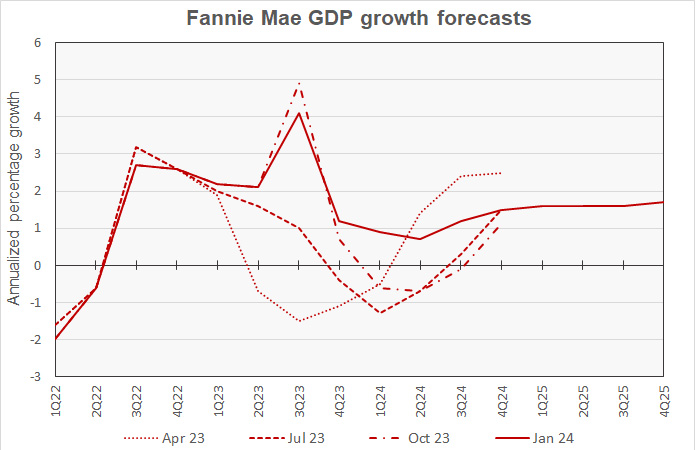

The next chart, below, shows Fannie Mae’s current forecast for Gross Domestic Product (GDP) growth, along with other recent forecasts.

While Fannie Mae is no longer predicting that the economy will shrink at some point in 2024, they still expect growth to slow during the year. The slowest growth is expected in Q2 2024 with predicted annualized growth of only 0.7 percent. However, this is much better than the 1.4 percent annualized contraction predicted in last month’s forecast.

The forecast predicts that the rate of growth will pick up slowly from Q3 2024 through the end of 2025. However, annualized growth is only expected to be 1.7 percent by Q4 2025, less than the Fed’s estimate of 1.8 percent long-term growth potential for the U.S. economy.

The full year forecast for GDP growth for 2023 was left unchanged at 2.6 percent. The full year GDP forecast for 2024 was revised upward by 1.4 percentage point to 1.1 percent. The GDP growth forecast for 2025 was revised downward by 0.1 percentage point to 1.6 percent.

Slower decline in inflation predicted

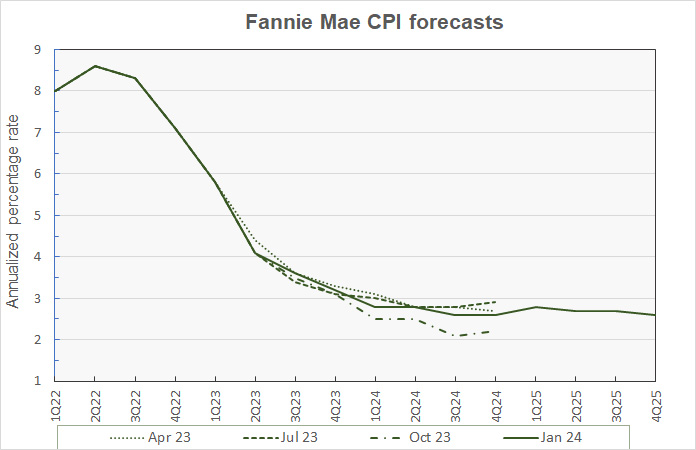

The next chart, below, shows Fannie Mae’s current forecast for the Consumer Price Index (CPI), along with three other recent forecasts.

Usually only small adjustments are made to the quarterly inflation projections from one monthly forecast to the next. However, in the January forecast, significant adjustments were made to the inflation projections for the last half of 2024. The predicted CPI inflation rate for Q3 was revised upward from 2.0 percent to 2.6 percent while the Q4 inflation rate was revised upward from 2.1 percent to 2.6 percent. It is notable that Fannie Mae’s forecast does not foresee inflation falling to the Federal Reserve’s target of 2.0 percent at any time through the end of 2025.

Looking at whole-year forecasts, the forecast for year-over-year CPI inflation in Q4 2024 was raised 0.5 percentage point to 2.6 percent. The Q4 2025 year-over-year inflation forecast was raised 0.1 percentage point to 2.6 percent.

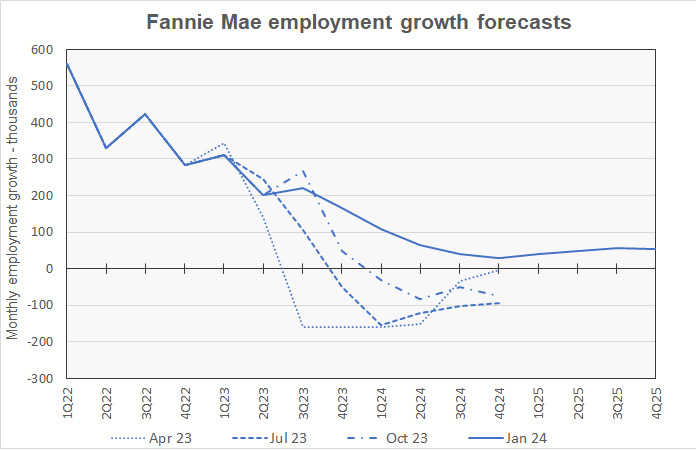

Continued employment gains predicted

The next chart, below, shows Fannie Mae’s current forecast for the employment growth, along with two earlier forecasts. Employment growth is our preferred employment metric since job gains, along with productivity gains, drive economic growth. By contrast, the unemployment rate depends on employment but also on the labor force participation rate. Either rising employment or falling labor force participation can drive the unemployment rate lower, but only the former would contribute to economic growth.

Given that Fannie Mae’s latest forecast no longer calls for GDP to shrink, it is not surprising that it also no longer calls for employment to decline. While it calls for employment growth to fall to an average of only 30,000 jobs per month in Q4 2024, this is well above the worst quarter for employment growth in last month’s forecast. That forecast called for an average loss of 99,000 jobs per month in Q3 2024.

Compared to last month’s forecast, the expected full year forecast for employment growth in 2023 was left unchanged at a gain of 2.7 million jobs. The employment growth forecast for 2024 was revised from a loss of 400,000 jobs to a gain of 700,000 jobs. The employment growth forecast for 2025 was revised from a gain of 300,000 jobs to a gain of 600,000 jobs.

The Fannie Mae January forecast can be found here. There are links on that page to the detailed forecasts and to the monthly commentary.