Yardi Matrix reported that national average apartment rent increased $5 in April to $1,709 per month. This is the largest monthly rent increase reported by Yardi Matrix since last July and indicates that a seasonal pick up in rents is underway this year after an unusually large decline in rents at the end of last year.

Year-over-year rent growth rates down despite rent rise

The national average asking apartment rent was up 3.2 percent in April from its year-earlier level. This rate of increase was down 0.8 percentage points from that reported last month. This marks 11 months in a row where the rate of year-over-year rent growth has declined.

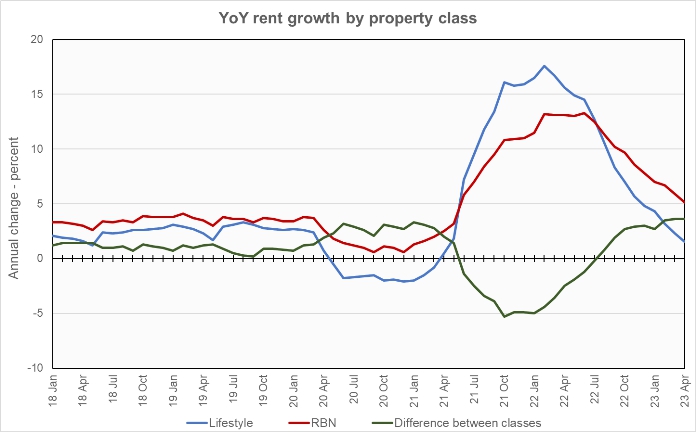

Rents in the “lifestyle” asset class, usually Class A properties, rose 1.5 percent year-over-year, while rents in “renter by necessity” (RBN) properties increased by 5.1 percent year-over-year. Both rates are once again lower than those reported for the prior month. The chart, below, shows the history of the year-over-year rent growth rates for these two asset classes along with the difference between these rates.

The chart shows that, while the year-over-year rent growth rates for both classes of apartments continue to fall, the difference between the rent growth rates has stabilized in the range it occupied during the first year of the pandemic. Rent growth for lifestyle properties is now below its average level in the two years leading up to the pandemic. However, rent growth for RBN properties is still well above its average level for that period.

The national average lease renewal rate was 64.0 percent February. This is up 0.1 percentage point from the initial value for January reported last month, but down from the revised level of 65.2 percent for January given in this month’s report. Year-over-year rent growth for leases that were renewed was 9.4 percent in February, up 0.1 percentage point for the month. This remains well above the rent growth rate for new leases, but Yardi Matrix expects these rates to converge over the course of the year as rents for renewed apartments catch up with those for apartments with new leases.

Yardi Matrix reported that U.S. average occupancy rate was nearly unchanged at 95.0 percent in March. Occupancy is down from the year-earlier level of 96.0 percent.

Yardi Matrix also reported that single-family rental (SFR) rents rose $10 in April to a level of $2,089 per month. The year-over-year rent growth rate for these properties fell to 2.3 percent. The national occupancy rate for single-family rentals in March was unchanged from the initial level reported for February at 95.5 percent.

Rent growth and more

Yardi Matrix reports on other key rental market metrics in addition to rent growth. These include the average rent to income ratio, the rent growth rate for residents who renew their leases and the portion of residents who do renew. The metro averages are included in the tables below, but the report also includes the rent to income ratios for both lifestyle and for RBN properties.

Of the top 30 metros by population, the 10 with the largest annual apartment rent increases as ranked by Yardi Matrix are given in the table below, along with their annual percentage rent changes, overall rent to income ratio, rent growth for renewed leases and renewal rate for the month. The data on asking rent growth is for April. The other data is for March.

| Metro | YoY asking rent growth % | Rent to income ratio % | YoY renewal rent growth % | Monthly lease renewal rate % |

| Indianapolis | 7.7 | 26.2 | 9.6 | 66.3 |

| Kansas City | 6.4 | 24.2 | 9.3 | 69.1 |

| New York | 6.2 | 33.4 | 16.2 | 64.0 |

| Boston | 5.2 | 28.1 | 7.9 | 64.8 |

| Chicago | 5.0 | 28.8 | 8.5 | 67.0 |

| Miami Metro | 4.5 | 27.4 | 13.7 | 70.2 |

| Philadelphia | 3.7 | 30.5 | 6.5 | 79.1 |

| Los Angeles | 3.6 | 32.1 | 12.2 | 46.5 |

| Portland | 3.5 | 30.8 | 11.0 | 60.3 |

| Charlotte | 3.4 | 29.1 | 10.3 | 62.7 |

The major metros with the smallest year-over-year apartment rent growth as determined by Yardi Matrix are listed in the next table, below, along with the other data as in the table above.

| Metro | YoY asking rent growth % | Rent to income ratio % | YoY renewal rent growth % | Monthly lease renewal rate % |

| Phoenix | (2.8) | 28.4 | 8.4 | 59.8 |

| Las Vegas | (2.5) | 30.3 | 8.9 | 63.8 |

| Seattle | (0.1) | 27.9 | 9.6 | 57.8 |

| Austin | 0.0 | 26.9 | 11.0 | 60.4 |

| Atlanta | 0.4 | 29.9 | 8.0 | 66.8 |

| San Francisco | 0.5 | 30.9 | 5.6 | 49.7 |

| Sacramento | 0.7 | 40.8 | 7.3 | 57.0 |

| Orange County | 0.8 | 32.4 | 9.5 | 63.9 |

| Tampa | 1.6 | 31.9 | 10.2 | 66.4 |

| Inland Empire | 2.1 | 30.6 | 9.6 | 57.9 |

The top metros for month-over month rent growth in April were Boston, New York and Raleigh. Twenty-one of the 30 metros tracked saw positive rent growth for the month, down 1 from last month. The metros with the lowest month-over-month rent growth were San Francisco, San Jose and Phoenix. An indication of the volatility of this metric is that two of the top three metros for rent growth and two of the bottom three metros for rent growth were not on those lists last month.

Risks to refinancing multifamily properties

The discussion section of the report last month dealt with financing issues due to bank stress. The discussion section of the report this month dealt with financing issues associated with property loans maturing and requiring refinancing. This was also the subject of a recent report from Trepp so refinancing risk is a significant current concern for the multifamily industry.

Yardi Matrix pointed out that multifamily finance is currently healthy with low rates of loan delinquencies. They also point out that properties with loans that were originated in 2020 or earlier have seen huge surges in their rents over the terms of those loans. This should allow them to support new loans, even with less favorable terms. Add in the presence of Fannie Mae and Freddie Mac as lenders of last resort, and there is reason to think that distress due to refinancing issues may be limited.

The report suggests that distress may be concentrated in submarkets that are weak due to high volumes of new deliveries or low rent growth due to rent control. Properties whose sponsors are unable to fill the capital gaps caused by tougher refinancing loan terms may also have issues.

Fewer SFR markets see gains

Yardi Matrix reported on the top 34 metros for single family rentals. This month, 21 of the 34 metros covered saw positive year-over-year rent growth, down 3 from last month’s count. The leading metros for year-over-year rent growth were Nashville, Baltimore and Chicago, the same as last month.

This month, only 4 of the metros saw year-over-year occupancy increases. These metros were Sacramento, Raleigh, Orlando and Atlanta. Washington D.C, Austin and Seattle saw the greatest SFR occupancy declines. The year-over-year occupancy decline in Washington D.C. was again over 10 percent.

The complete Yardi Matrix report provides information on some of the smaller multifamily housing markets. It also has more information about the larger multifamily markets including numbers on job growth and completions of new units. It includes charts showing the history of rent changes in 18 of the top 30 markets over the last 4 years. It can be found here.